Key takeaways:

- Research suggests M&A deals may fail to deliver expected value 70-75% of the time.

- Common culprits often include preventable issues: messy financials, customer concentration, missing compliance documentation, and poor integration planning.

- Evidence indicates that sellers who commission Quality of Earnings reports may achieve higher multiples, while those who address potential deal-breakers proactively can be better positioned to negotiate from strength.

Imagine, as a founder, watching twelve months of preparation unravel in forty-eight hours. Your buyer’s due diligence team had uncovered what they called “customer concentration risk”: a significant portion of annual revenue concentrated among just a few customers. Within days, the offer falls through. The deal was not dead because the business was failing. It appears to have died because the risk was invisible to the seller but blindingly obvious to the buyer.

This pattern may repeat itself numerous times each year across mid-market M&A. According to research analysing 40,000 transactions over four decades, an estimated 70% to 75% of M&A deals may fail to deliver expected value based on the researchers’ methodology. While headlines blame market conditions or cultural mismatches, common culprits can be far more pedestrian: messy financials, missing compliance docs, customer concentration, and integration blind spots that sellers could potentially have fixed months before going to market.

The good news? Many M&A deal breakers may be fixable. The bad news? Some sellers discover them during due diligence, when it can be too late to negotiate from strength.

Financial chaos: When the numbers do not tell the truth

Buyers often do not trust unaudited management accounts, and experienced advisors suggest they may be right to exercise caution. In one reported case, a private equity firm nearly acquired a company with significant reported EBITDA, only for their Quality of Earnings analysis to reveal that a substantial portion allegedly came from one-time asset sales. The sustainable EBITDA was reportedly considerably lower, potentially saving the buyer from overpaying significantly.

This is why Quality of Earnings reports have become increasingly common in professional M&A. Many buyers reportedly rank unreliable financials as among the top deal concerns, and they may assume aggressive add-backs, misclassified expenses, or revenue recognition issues until proven otherwise. If your recent trading shows a downturn during exclusivity, buyers may either seek to reduce the price or consider walking entirely.

Potential fix: Consider commissioning a sell-side QoE report 3 to 6 months before launching a sale process. Costs can vary significantly, typically ranging from £15,000 for smaller deals to £100,000 or more for complex transactions, depending on deal complexity and provider. Clean up obvious issues: remove personal expenses from the P&L, reconcile management accounts to statutory filings, and tighten working capital reporting. According to GF Data research, in their sample, sellers using sell-side QoE saw TEV/EBITDA multiples of 7.4x on average, compared with 7.0x for those that did not, suggesting the investment may often pay for itself, though individual results will vary

Customer concentration: The silent valuation killer

Here is a potentially uncomfortable truth: many industry practitioners suggest that if one customer represents more than 15-20% of your revenue, or your top five accounts for approximately 30-40%, you may have a concentration concern worth addressing. And concentration issues can potentially reduce transaction valuations by an estimated 20% to 35%, according to industry sources.

Many buyers may see customer concentration as fragility dressed up as loyalty. One contract loss, one acquisition of that customer by a competitor, one relationship breakdown, and the business value could potentially decline significantly. Some financial buyers may be reluctant to pursue deals with high concentration, and some banks may be hesitant to finance them, potentially forcing buyers to use more cash and possibly reducing your leverage at the negotiating table.

Potential fix: Consider mapping revenue by customer, product, and contract term at least six months before sale. Strengthen key relationships by renewing contracts early, extending terms, and reducing termination-at-will risk. Where concentration is unavoidable, build a mitigation story: show multi-year history, evidence of embeddedness, and pipeline of new logos. Companies with tenured relationships and deep integration across operational channels may be able to significantly mitigate perceived risk in buyers’ eyes.

Integration concerns: Can this business actually be plugged in?

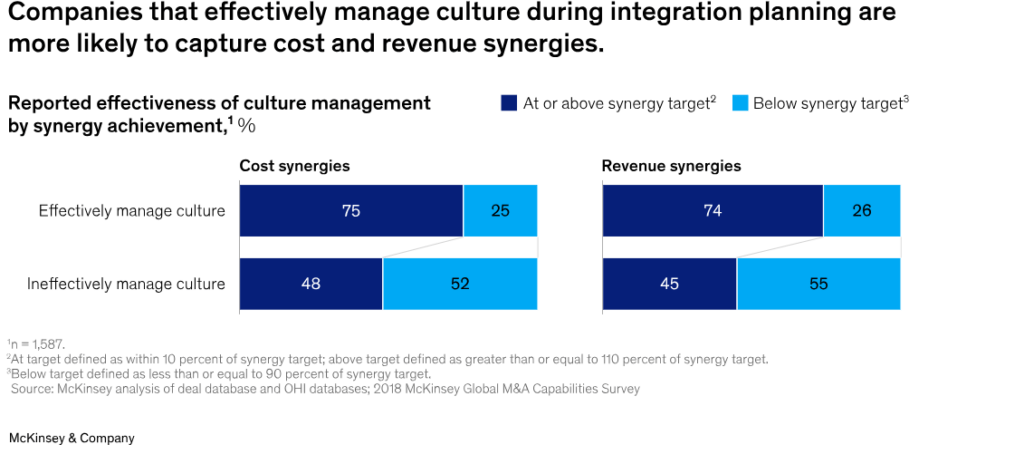

Research from McKinsey suggests that poor integration and cultural misfit may destroy significant M&A value. According to McKinsey research, companies that manage culture effectively in their integration planning may be around 50% more likely to meet or exceed their synergy targets. Buyers may walk if they conclude integration could be too complex, too costly, or too slow to realise synergies.

Source: McKinsey & Company

If your business is held together by tribal knowledge, undocumented processes, and key-person dependencies, you may have handed buyers a significant concern. They are not buying a company; they could be buying a future integration headache.

Potential fix: Consider making your business as “plug-and-play” as possible. Document core processes, create clear organisation charts, standardise systems, and establish transparent KPIs. Identify key people and design retention plans so buyers believe the capability they are acquiring will stay. Understanding how to navigate post-merger integration from day one can make your business significantly more attractive to potential acquirers.

Three potentially valuable strategies to consider

1. Vendor due diligence: Seeking to identify issues before buyers do

Vendor due diligence simulates buyer scrutiny on your financial, legal, tax, and commercial position, so you may discover and fix issues before buyers raise them as concerns. Industry experience suggests that deals where issues emerge during diligence can experience price reductions, restructurings, or walk-aways, precisely what VDD aims to help prevent. For businesses considering a comprehensive company purchase advisory, understanding the buyer’s diligence perspective is essential.

2. Data room preparation: Professionalism can signal credibility

A structured data room can signal professionalism and may reduce unknowns that concern buyers. Poor, disorganised data is often cited as a common deal obstacle. Consider building standard folder structures, ensuring all documents are scanned and labelled, enabling version control, and creating FAQ documents explaining numbers upfront.

3. Contract standardisation: consistency can support predictability

Patchwork contracts with custom terms can create risk and integration headaches. They may also make it more difficult for buyers to model revenue durability. Consider creating standard templates for customer, supplier, and employment contracts. Review key contracts and amend where possible to reduce at-will termination, clarify change-of-control consequences, and align payment and liability terms.

When to start

Many of the companies that secure strong valuations and smooth exits reportedly treat deal preparation as a 3- to 6-month strategic project, not a last-minute scramble. They may commission QoE reports, run legal and IP audits, clean cap tables, and de-risk customer concentration long before entertaining buyer interest.

The deals that struggle, the ones that can leave sellers frustrated and exhausted, may be the ones that gambled on hope. They may have assumed buyers would not notice the cracks. In many cases, they appear to have been wrong.

For businesses exploring their options, understanding accurate business valuation methods is a crucial first step. In uncertain markets, creative deal structuring may help overcome identified weaknesses, but typically only if those weaknesses are addressed proactively rather than discovered reactively.

The choice is yours

M&A transactions may not be won or lost at the negotiating table. They can be significantly influenced by the months of preparation that precede the first buyer meeting. Many of the businesses that achieve premium valuations, favourable terms, and successful closings appear to be the ones that ran vendor due diligence, cleaned financials, de-risked customer concentration, documented processes, and built trust through transparency.

Consider beginning your preparation early with Acquinox Advisors: because by the time a buyer’s due diligence team uncovers issues that could have been addressed, it may be too late to negotiate from strength.

Frequently Asked Questions

What is the most common reason M&A deals fail to deliver expected value?

Research suggests that poor integration planning and cultural misalignment are among the most significant factors. However, preventable issues such as unreliable financials, customer concentration, and inadequate due diligence preparation also frequently derail transactions or reduce valuations.

How much does a Quality of Earnings report cost?

Costs vary based on business complexity and deal size. For smaller mid-market transactions, expect to pay approximately £15,000-£35,000, while larger or more complex deals can cost £60,000-£100,000 or more. Despite the investment, research suggests sellers who commission QoE reports often achieve higher valuation multiples.

At what level does customer concentration become a deal concern?

Most buyers consider any single customer representing more than 15-20% of revenue as a concentration risk. When a customer exceeds 20%, expect detailed questions; above 30%, concentration typically becomes a significant deal factor that may affect valuation or deal structure.

This article has been prepared by Acquinox Advisors using data from public sources as linked. This content is for informational purposes only and does not constitute financial, legal, or investment advice. Readers should consult qualified professional advisers before making business sale decisions.