Private equity deal value hit $2.6 trillion in 2025, with entry multiples reaching record highs of 11.8x EBITDA. Business owners choosing between a full exit and rollover equity face a complex decision: take guaranteed liquidity now, or bet on a “second bite” that could generate more total wealth, if growth materialises. We examine when rollover works, when it doesn’t, and what protections to negotiate.

Picture this: Your phone rings. It’s a private equity firm with a number big enough to change your life. But there’s a twist. They want you to roll 30% back into the deal and bet on tomorrow. You built this business from scratch. Now you’re being asked to stay invested with someone else at the wheel. So what do you do? Take the money and run, or double down for a second payday that could dwarf the first?

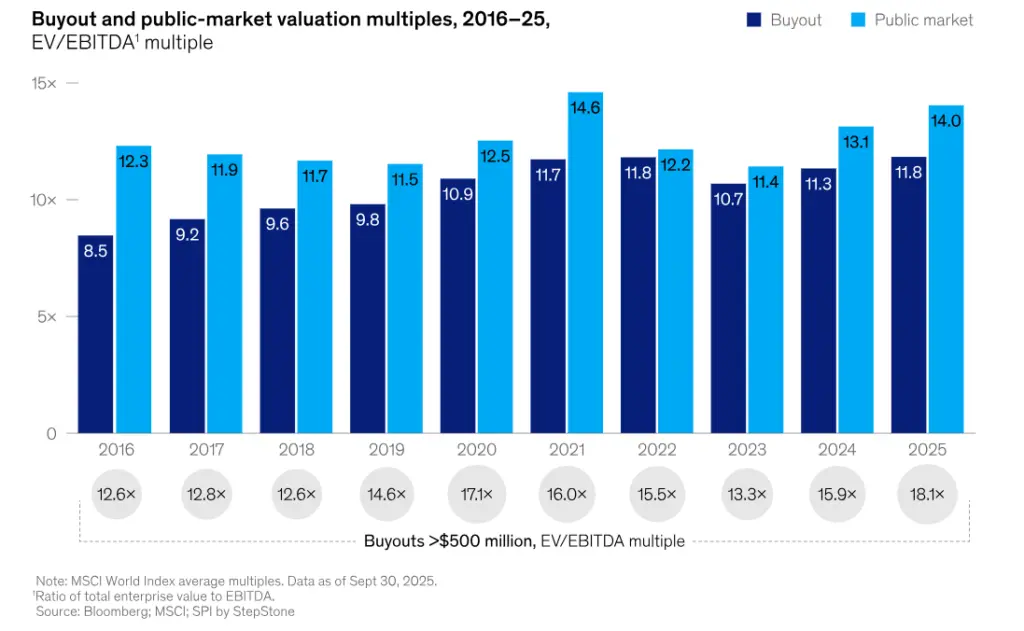

Private equity surged in 2025 with deal volumes hitting $2.6 trillion, and holding periods stretching to an average of 6.6 years as firms navigate tighter exit markets. Purchase multiples reached record highs of 11.8x EBITDA, fundamentally changing how business owners think about exits. For founders evaluating their options, the decision between cashing out completely or taking partial liquidity with rollover equity has never been more consequential.

Source: McKinsey

What’s really on the table

Let’s cut through the jargon. A full exit means selling 100% of your business and walking away with a cheque. Clean, simple, done. A partial sale with rollover equity means taking cash for most of your stake while keeping skin in the game for round two.

The rollover trend is accelerating. Average rollover equity contribution hit 6% in Q1 2025, higher than the previous five-year range of 1-3%. In middle-market deals, 20-30% rollover has become standard practice. Private equity buyers prefer it because it keeps you invested in the outcome. You might also prefer it because it opens the door to wealth multiplication.

But here’s the catch. That second bite only tastes sweet if the business grows.

The full exit: certainty over upside

Selling everything gives you maximum control over one thing: getting out. Financial buyers often pay the richest multiples. Private equity buyers paid a median 12.8x EBITDA in the US versus 9.9x for corporate acquirers, but both offer immediate liquidity and a definitive endpoint.

You de-risk everything. Market crashes, competitive threats, operational nightmares? Not your problem anymore. You convert an illiquid asset into diversified investments or fund retirement on your terms.

The downside is equally clear. If your business triples in value under new ownership, you don’t see a penny. You’ve capped your upside permanently. And for many owners, watching their company flourish without them creates profound regret. According to the Exit Planning Institute, approximately 75% of business owners experience profound regret within the first year after selling.

The rollover play: betting on tomorrow

Most private equity firms structure deals expecting the seller to reinvest. They’ll buy 60-80% of your company and ask you to roll the rest into the new entity. Three to five years later, they sell again. Your minority stake rides that wave.

Here’s how wealth multiplication works in practice, using illustrative UK tax assumptions:

Assumptions:

- Enterprise value: £120 million (equity value, minimal debt)

- Your cost basis: £20 million (original investment)

- Structure: Sell 70% for cash, roll 30% tax-deferred

- UK tax: Business Asset Disposal Relief (£1m at 10%) + 20% capital gains tax on remainder

| Full Exit Today | 70% Sale + Rollover | |

| Cash proceeds | £120m | £84m (70%) |

| Less: Cost basis | £20m | £14m (70% of basis) |

| Taxable gain | £100m | £70m |

| Tax payable | £19.9m | £13.9m |

| Net cash received | £100.1m | £70.1m |

| Rollover equity value | £0 | £36m (30%, tax deferred) |

Important: This illustration assumes tax deferral on the rolled portion under share-for-share exchange relief in the UK. Individual circumstances vary significantly and country by country. Consult a qualified tax advisor.

When the maths breaks down

EBITDA growth must materialise. Multiple expansion isn’t guaranteed. Market data suggests companies being exited can sell at lower median multiples than those still held in portfolios during challenging exit environments. If the business stagnates or contracts, your rolled equity shrinks or evaporates.

Exit timing matters more than ever. Holding periods now average more than 6 years globally, with a significant portion of companies held for four years or longer. Your expected three-to-five-year hold could stretch to seven or eight. That’s a long time to wait for liquidity, especially if you’re nearing retirement.

And then there’s leverage. Private equity-backed companies typically carry higher debt loads. Median debt multiples have fluctuated, with debt-to-EBITDA ratios for US LBOs now hovering around 5x. More debt means more risk if performance wobbles.

The risks you can control

Smart owners negotiate protections upfront

- Tag-along rights: Ensure you can exit when the PE firm does

- Drag-along rights: Prevent you from being forced to stay if the PE wants to hold

- Board seats or observer rights: Give you visibility into decisions

- Anti-dilution provisions: Protect against future fundraising rounds that could shrink your stake

- Preferred return hurdles: Clarify whether your equity ranks pari passu with the PE firm’s equity

Governance also matters immensely. As a minority shareholder, you no longer control the company. The private equity firm makes final calls on strategy, hiring, capital allocation, and exit timing. If you don’t trust them, don’t roll equity.

Conduct due diligence on the buyer as rigorously as they conduct it on you. Check their track record with similar businesses. Talk to other management teams who rolled equity with this firm. Understand their typical value creation playbook and whether it fits your company’s needs.

What about your life?

Financial modelling only tells half the story. How close are you to retirement? Do you need immediate liquidity to pay off debt or diversify your wealth? Are you ready to walk away completely, or would you miss the daily challenge of building something?

For owners who aren’t ready to let go, a partial sale offers continued involvement without the full risk and burden of ownership. The private equity firm typically handles back-office operations, M&A execution, and capital raising. You focus on what you do best: running the business.

But if you’ve been dreaming of that clean break for years, don’t let spreadsheets talk you into staying. Money isn’t everything. Peace of mind and freedom have value too.

The market right now

Private equity firms are sitting on record dry powder exceeding $1.7 trillion globally as of the end of 2025. With interest rates stabilising and exit markets showing signs of recovery, the stage is set for increased deal activity. For sellers, this creates a favourable negotiating environment.

Entry multiples are high. Traditional drivers of PE returns like cheap leverage and multiple expansion have largely been spent. That means private equity firms must rely heavily on operational improvements to hit their return targets. Your confidence in their ability to execute becomes critical to the rollover decision.

Exit markets showed improvement in 2024 and 2025 but remain well below historical norms. The backlog of companies awaiting exit continues to grow. That doesn’t mean you shouldn’t roll equity, but it does mean you should plan conservatively on timing.

Which path creates more wealth: immediate exit or partial rollover?

It depends entirely on execution. If the business grows meaningfully and exits at a premium multiple five years from now, the rollover strategy wins decisively. You could generate more total wealth than selling everything today.

If the business flatlines or deteriorates, you would have been better off taking the full exit. That portion you rolled could have been safely invested elsewhere, compounding with far less risk.

Think of it as portfolio allocation. What percentage of your net worth are you comfortable leaving in this one asset? For some owners, 30% makes sense. For others, zero is the right answer. There’s no universal rule.

The strongest candidates for rollover equity have:

- High confidence in growth trajectory

- A capable private equity partner with relevant industry experience

- Strong governance protections negotiated upfront

- Adequate liquidity from the cash portion to meet personal financial needs

- Appetite for continued involvement in the business

The strongest candidates for full exit have:

- Immediate liquidity requirements for retirement or estate planning

- Low risk tolerance for continued business exposure

- A business at maturity with limited growth runway

- Desire for a complete break from operations

- Current market valuations at or near peak levels

Speak to a qualified advisor rather than deciding on a hunch

The second bite can be sweeter than the first, but only if the apples keep growing. Rollover equity turns a single transaction into a multi-stage wealth creation event. When it works, it works brilliantly. When it doesn’t, you’ve tied up significant capital in an illiquid, minority position with no control over outcomes.

Work with experienced M&A advisors who can model scenarios, identify risks, and negotiate protections that matter. The difference between a good deal and a great one often comes down to what’s negotiated in the months before signing.

At Acquinox Advisors, we specialise in helping business owners navigate these exact decisions. Whether you’re preparing your company for sale or evaluating an incoming offer, we ensure you enter the negotiation room with clarity and confidence. Contact us today for more information.