Key takeaways:

- Know your buyer type: Strategic buyers pay for synergies; financial buyers pay for scalable, clean assets

- Position your business as “plug and play”: Clean financials, strong KPIs, reduced founder dependency, and a credible growth story

- Run a competitive process: Build a buyer map, tailor your pitch, and create tension through parallel bidding

- Act now: 2026 may present a favourable exit window.

In early 2026, private equity firms are sitting on record dry powder exceeding $1.7 trillion globally. Middle-market deals may present significant opportunities as buyers seek quality assets. Yet many business owners still approach their exit the same way: they wait for the phone to ring, field an unsolicited offer, and hope for the best. In some cases, the valuation disappoints, or the deal falls apart during due diligence.

The owners who tend to achieve premium exits don’t rely on luck. They work to engineer it. They decide who they want to attract, deliberately shape the business around what those buyers tend to value most, and orchestrate a competitive process that can help put leverage back in their hands.

Table of contents

- Why strategy beats “Wait and See”

- Strategic vs financial buyers: Know your audience

- Four positioning pillars that can command premium multiples

- Engineering competitive tension: The controlled auction

- What can kill deals

- The 2026 window may be open

- Ready to explore how to maximise your exit value?

- Frequently Asked Questions

Why strategy beats “Wait and See”

Listing your business and waiting for buyers can be like hosting a silent auction where nobody knows they’re bidding. A structured sell-side strategy can help flip the script by doing three things.

First, it can help pre-empt surprises. Vendor due diligence allows sellers to identify and address issues before buyers uncover them, potentially reducing re-trades and building confidence. Clean financials, organised data rooms, and proactive explanations tend to signal professionalism and may reduce perceived risk.

Second, it can help curate your audience. Instead of broadcasting to anyone with a chequebook, disciplined sellers can target the strategics and financial buyers with the highest strategic fit, the ones who may be willing to pay not just for today’s cash flow, but for the growth they believe they can unlock with their own capital, distribution, or operational leverage.

Third, it can help create tension. Competitive deal processes may encourage buyers to sharpen their terms. Multiple motivated bidders can potentially increase price, improve deal certainty, shorten timelines, and reduce your exposure to aggressive renegotiation.

Strategic vs financial buyers: Know your audience

Not all buyers see value through the same lens. Understanding the difference between strategic vs financial buyers can potentially add significant value.

| Strategic Buyers | Financial Buyers | |

| Who they are | Operating companies: competitors, adjacent players, customers, or suppliers | Private equity firms, family offices, search funds |

| Primary driver | Synergies (cross-selling, supply chain consolidation, competitor elimination) | Return on invested capital |

| Typical hold period | Long-term/permanent integration | Approximately five to seven years |

| What they value | Product fit, market access, cultural compatibility | EBITDA quality, scalability, management team strength |

| Premium trigger | Identifiable cost savings or revenue synergies | Clean books, proven processes, clear exit routes |

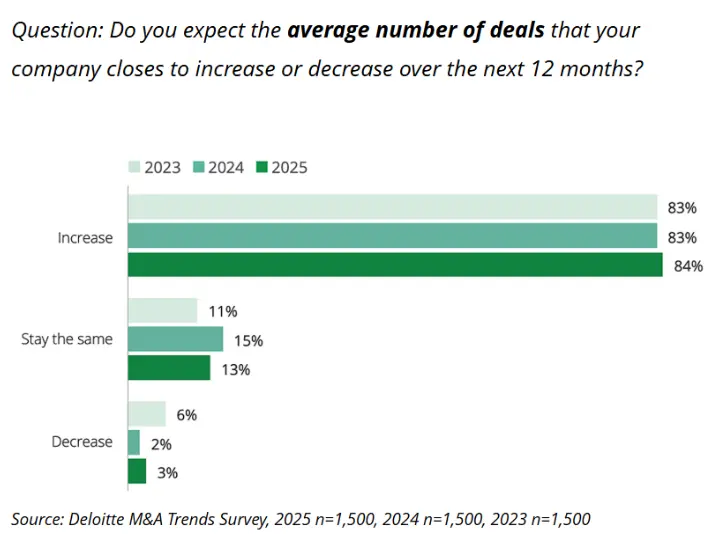

More than 80% of dealmakers surveyed expect to close more deals with greater value in 2026, with strategic acquirers appearing particularly active in sectors where operational integration may drive value.

Source: Deloitte

Four positioning pillars that can command premium multiples

High-value exits often look like plug-and-play assets. The following four elements can help drive higher valuations in many cases.

1. Clean, credible numbers

This is widely considered table stakes. Three years of monthly P&L, balance sheet, and cash flow reconciled to statutory accounts. A normalised EBITDA schedule with a transparent add-back bridge for owner comp, one-offs, and personal expenses. No surprises on debt, leases, or related-party transactions.

A sell-side quality-of-earnings review can help address weak spots before buyers see them. Clean numbers tend to build trust; messy numbers may trigger discounts or walkaways.

2. Strong KPIs that tell a story

Buyers generally want dashboards, not detective work. Revenue growth, gross margin, EBITDA margin, and cash conversion should ideally be visible at a glance, monthly, over 12 to 36 months. Consider adding cohort metrics where relevant: retention, churn, LTV/CAC, ARPU.

Transparency often matters more than perfection. If retention dropped in Q2, explain it. If margins improved in Q3, show what you did. Buyers tend to reward honesty, not spin.

3. Scalability without you

Reducing founder dependency through proper due diligence may boost EBITDA multiples by for smaller businesses, according to some industry analyses. Documented processes for sales, delivery, finance, and HR can help demonstrate that growth won’t break the business.

Systems matter too. Can your CRM, ERP, and accounting platforms export clean data? Can they integrate with a buyer’s stack? The easier you make integration, the less risk they may price in.

4. A growth story they can believe

Buyers often pay up for believable upside. Consider preparing three to five tangible initiatives, such as new geographies, verticals, products, pricing strategies, with rough impact and timing. Evidence that these levers already work at a small scale can strengthen your case.

Frame it from the buyer’s perspective. Targeting a strategic buyer? Show how you could cross-sell into their base or leverage their distribution. Targeting PE? Show margin improvement levers and EBITDA expansion tied to operational upgrades.

Engineering competitive tension: The controlled auction

Strategy without execution is just a plan. Many successful exits involve a structured, competitive process that encourages buyers to move in parallel and bid competitively.

Build your buyer map

Consider starting with 15 to 40 high-fit buyers: strategics (competitors, adjacencies, customers, suppliers) and financial buyers (PE firms, family offices active in your sector and size range). For each, note the strategic rationale:” fills UK gap,” “adds SaaS SKU,” “vertical integration.”

Rank them in A and B tiers by fit, acquisition history, culture, and integration track record.

Tailor the pitch

Generic teasers may represent missed opportunities. Strategics tend to care about synergies, product fit, market access, and cultural compatibility. Financials generally care about EBITDA quality, cash flow, scalability, and exit routes.

The core data can be common, but the story should ideally be tuned. One PE firm might care about recurring revenue; another might care about add-on opportunities for their platform company.

Run a disciplined process

Readiness → indicative offers → shortlist → management meetings → letters of intent → exclusivity.

Send teasers, then NDAs, then confidential information memorandums in waves. Consider setting firm deadlines for bids to encourage buyers to move in parallel.

Use feedback to refine positioning and gently signal other interest. This approach can also help manage earnouts and contingent consideration more effectively.

What can kill deals

Certain repeating patterns can doom exits. Consider avoiding these.

No clear buyer type → weak positioning. Sellers who talk to “everyone” may find that their narrative becomes generic. Strategics may not see synergies; financial buyers might not see a scalable asset.

Owner-centric business → PE may walk. Financial buyers can step back when everything runs through the founder. They may not see how the business performs without you.

Under-prepared financials → serious buyers may disappear. Sloppy books and missing data can undermine confidence. Quality buyers may either re-price aggressively or choose not to bid at all.

No growth story → primarily bargain hunters may engage. Businesses marketed as static cash cows can attract bottom-fishers, not strategic acquirers who might pay premiums for future upside.

The 2026 window may be open

According to recent industry reports, the M&A market appears to have momentum. PE firms are sitting on a large pile of idle cash allocated for buyouts. Following three rate cuts in late 2025, interest rates have moderated somewhat, though they remain elevated relative to the past decade. Some analysts suggestvaluation gaps may be narrowing, with record PE capital and strategic sector moves expected by some analysts to support M&A activity through 2026, though market conditions can change rapidly.

Companies operating in technology, healthcare, and financial services may be well-positioned to explore exit opportunities while the supply side appears constrained and buyers appear active. For owners considering an exit in the next 12–24 months, it may be prudent to begin preparation now.

Ready to explore how to maximise your exit value?

Building an M&A strategy that can help attract premium buyers and encourage competitive bidding typically requires expertise, market intelligence, and disciplined execution. At Acquinox Advisors, we work with middle-market business owners through every stage of the sell-side process, from comprehensive due diligence and positioning to buyer outreach and deal negotiation.

Whether you’re exploring a strategic sale or evaluating financial buyer options through private equity advisory, our team brings sector expertise and experience in helping clients work towards maximising transaction value.

Contact us at Acquinox Advisers today to discuss your exit strategy and explore how we may be able to help you work towards the outcome you deserve.

Frequently Asked Questions

How long does a typical M&A process take from start to close?

A well-prepared sell-side process typically takes 6–12 months from initial preparation to close, though complex transactions or difficult market conditions can extend timelines. Early preparation, including financial clean-up, due diligence readiness, and buyer mapping, can help compress the active marketing phase.

What’s the difference between a strategic buyer premium and a financial buyer’s offer?

Strategic buyers often pay higher multiples because they’re acquiring synergies (cost savings, revenue opportunities, competitive positioning) they can realise through integration. Financial buyers typically base valuations on standalone cash flow and achievable operational improvements within their hold period. The right buyer depends on your priorities: maximum price, cultural fit, employee outcomes, or ongoing involvement.

When should I start preparing my business for sale?

Ideally, 18–24 months before your target exit date. This allows time to address financial clean-up, reduce founder dependency, strengthen your management team, and document key processes. However, market windows can shift, so maintaining “exit readiness” as an ongoing discipline is increasingly valuable.

This article has been prepared by Acquinox Advisors using data from public sources as linked. This content is for informational purposes only and does not constitute financial, legal, or investment advice. Readers should consult qualified professional advisers before making business sale decisions.