Key insights:

- SaaS buyers in 2026 are paying for quality, not just growth. Companies with Rule of 40 scores above 50% and Net Revenue Retention (NRR) above 110% are commanding significant valuation premiums over peers focused solely on top-line growth.

- The gap between average and exceptional outcomes is widening. Based on recent McKinsey SaaS research, efficient growth and durable unit economics now matter more than raw ARR velocity.

- Vertical specialisation and genuine AI integration attract strategic premiums, while AI-driven commoditisation threatens undifferentiated horizontal software.

Consider this scenario: Two SaaS companies, both with $10 million ARR. Same market. Same quarter. One exits at $40 million. The other at $82 million. While hypothetical, this type of 105% differential is not uncommon for what looks, on paper, like identical businesses.

What separates them is rarely luck or timing. It’s metrics. The second founder understood that in 2026, buyers increasingly focus on more than revenue alone. They pay for quality, efficiency, and defensibility. The gap between those who recognise this shift and those who don’t is wider than in recent years.

Current market context

Industry data suggests SaaS M&A volumes remain elevated entering 2026, yet valuation premiums are concentrating among a shrinking pool of top performers. While some companies command double-digit multiples, a larger share of transactions cluster at low single-digit outcomes. The market is sorting itself out.

From growth-at-all-costs to sustainable profitability

The Rule of 40 (that a healthy SaaS company’s revenue growth and profit margin should add up to 40% or more) used to be considered a safety net. Hit it, and you were generally safe from pressure to sell. That dynamic is shifting. AI has changed the equation, with software companies facing growing pressure from AI-driven commoditisation.

The implication for SaaS founders is significant: near-term profitability alone may not suffice in 2026. Many companies already live under the threat that AI could render their distinctive capabilities less distinctive, despite profitability.

The market has fundamentally reset from “growth at all costs” to “disciplined, specialised efficiency.” Learn more about how we assess these metrics in our valuation and financial modelling practice.

The metrics that move multiples

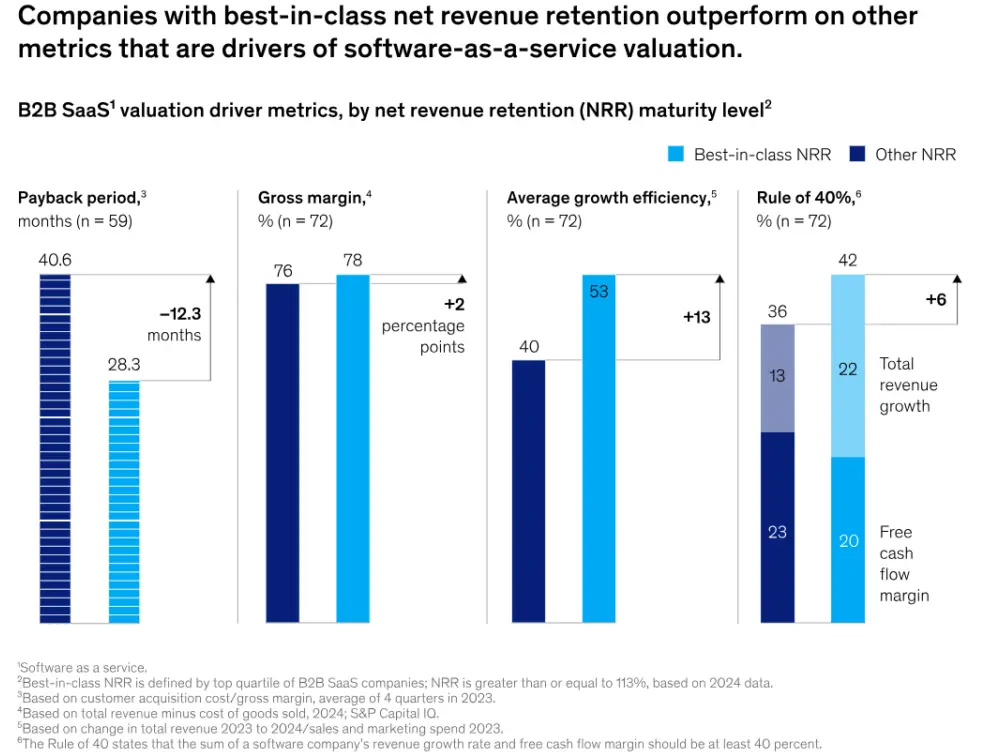

If you ask ten SaaS founders what drives their valuation, most will say ARR growth. Fewer will mention profitability. Almost none will start with net revenue retention. Yet NRR is widely considered one of the strongest predictors of premium valuations in current market conditions.

Market analysis consistently shows that companies with best-in-class NRR, often exceeding 113%, can command a substantial premium on their valuation multiples compared to peers with flat retention. In illustrative terms, for a company with $10M in ARR, this premium alone can translate into tens of millions of dollars in additional enterprise value at exit.

Why? Because NRR compounds. Theoretically, a company with 120% NRR that stopped acquiring new customers entirely could still grow its $10M ARR base to nearly $25M over five years just from their existing customer base. Buyers understand this arithmetic better than most founders.

The other metrics that often separate premium exits from average ones include (approximate numbers): gross margin above 75%, customer acquisition cost payback under 12-18 months, LTV:CAC ratios above 3:1, and annual gross churn below 5-10% for enterprise segments.

Evidence suggests that a higher Rule of 40 score is strongly correlated with a higher EV/Revenue multiple. While the impact varies, some market analyses indicate that a 10-point improvement in the score can lead to a notable uplift in the valuation multiple.

Source: McKinsey

AI integration: A valuation factor

Many buyers in recent industry reports indicate paying valuation premiums for AI-native or deeply integrated AI companies. But buyers have gotten sophisticated about separating real AI value from AI marketing.

What buyers actually look for: AI showing up in retention and expansion metrics, system-wide integration rather than isolated tools, and demonstrated improvements in gross margin or cost-to-serve.

The flip side: AI-driven commoditisation is increasingly viewed as a significant risk to SaaS valuations. AI has compressed the time, cost, and expertise required to build software, allowing small teams to create credible, competitive products in weeks. Buyers are actively discounting feature-based moats and paying for data depth, workflow lock-in, and proprietary datasets that create durable differentiation.

The risks that compress valuations significantly

Four factors often negatively impact SaaS valuations during due diligence, regardless of strong headline metrics:

- Customer concentration: When a single customer represents more than 10-15% of ARR, buyers apply material valuation discounts or structure deals with earnouts tied to customer retention.

- Weak data infrastructure: Companies with unreliable financial reporting, missing cohort analysis, or inability to produce clean NRR calculations face deal delays or termination. Sophisticated buyers view data quality as a proxy for operational competence.

- Founder-led sales dependency: When revenue generation revolves around the founder’s personal relationships, buyers perceive key-person risk. The solution involves building a sales process that is auditable, repeatable, and defensible without the founder’s direct involvement.

- High churn masking growth: Companies with annual gross churn above 10% in enterprise segments or above 20% in SMB segments face material valuation discounts unless offset by exceptional expansion revenue.

What founders should consider now

If you’re building toward an exit in the next 18-24 months, the preparation work with the highest ROI is often not hiring an investment banker six months before you want to sell. It’s improving the metrics that drive multiple expansion right now.

A10-point NRR improvement could potentially translate to a 20-30% valuation increase. Illustratively, at $5M ARR, that could represent $5-10M in additional exit value. A 12-month investment in reducing churn and improving expansion revenue can add 1-2x to your exit multiple.

Companies achieving premium outcomes in current market conditions share common characteristics: NRR above 110%, Rule of 40 scores above 50%, gross margins above 75%, clean financial reporting with quarterly-updated data rooms, sales processes independent of founder relationships, and either genuine AI integration that improves unit economics or defensible vertical specialisation.

For those considering buy-side opportunities, the same metrics apply in reverse: buyers who understand what drives sustainable value can identify mispriced assets in a market where many sellers still optimise for vanity metrics.

To conclude

The market has gotten selective. And that selectivity rewards preparation, operational excellence, and understanding what buyers actually value versus what founders think they value.

In 2026, the gap between those two perspectives could be worth millions.

If you’re a SaaS founder preparing for M&A, the question is not whether your company is valuable. It’s whether you’re measuring and optimising for the metrics that translate into premium outcomes. Because in a market where the spread between average and exceptional is wider than in recent memory, strong performance is rewarded, and increasingly essential for achieving value creation in M&A. Connect with our M&A specialists to discuss how these market dynamics apply to your specific situation and what strategic preparation could unlock in enterprise value.