Key Takeaways

- Process beats luck: Research suggests approximately 70–75% of M&A deals may underperform expectations — the difference between success and failure often lies in having a repeatable buy-side playbook.

- Strategy first: Define what you need (market, technology, talent, geography) before screening targets.

- Triangulate valuation: Use DCF, comparables, and precedent transactions to establish a fair value range and walk-away price.

- Plan integration early: Leading acquirers now plan operating models before due diligence — wiring integration assumptions directly into deal terms.

Many acquisitions struggle not because of bad targets, but because of inadequate process. With research suggesting approximately 70–75% of M&A deals may underperform expectations, the difference between success and failure often lies in having a repeatable buy-side playbook. As deal activity surges and mid-market opportunities multiply, disciplined acquirers with clear frameworks may be better positioned to capture value while others risk overpaying and stumbling through integration.

The price of winging it

Consider this scenario: Two companies announce acquisitions on the same Monday. Both pay similar multiples. Both tout synergies. Eighteen months later, one has captured most of its promised value, retained key talent, and accelerated growth. The other is bleeding customers, has lost half its leadership team, and is quietly writing down goodwill.

What separated them may not have been luck. It was likely a process.

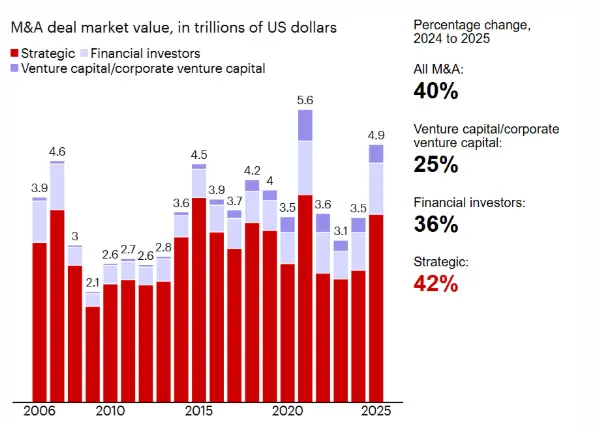

Buy-side M&A isn’t rocket science, but it does require discipline. Studies indicate over 70% of deals may fail to meet objectives. 2025 delivered a dramatic M&A rebound, with deal value surging approximately 40% to $4.9 trillion. Yet while mega-deals grabbed headlines, there may be significant opportunities in 2026 elsewhere, with small and medium-sized deals potentially presenting meaningful opportunities for prepared buyers willing to execute with discipline.

Image Credit: Bain & Co.

Stage one: Strategy before targets

Many acquirers start by asking “What’s for sale?” More successful acquirers often start by asking “What do we need?” Your acquisition thesis should ideally answer four strategic dimensions before you screen a single company:

Market dimension: Which segments or geographies must you win? Be specific. “B2B SaaS companies in DACH with €10–50 million revenue and 15–25% growth” is strategic. “Fast-growing tech companies” is not.

Technology and capability dimension: What’s missing from your organisation today? Are you buying AI talent you can’t hire fast enough? Cloud-native architecture to replace legacy systems? Data infrastructure for an ecosystem play? Articulate the gap clearly.

Talent dimension: Are you acquiring teams as much as products? For knowledge-intensive businesses, leadership quality, engineering depth, and low founder dependency can often matter more than the revenue line.

Geography dimension: Where do you need licences, local relationships, or physical presence that’s too slow or expensive to build?

If a target doesn’t clearly advance at least one of these four dimensions and meet your financial hurdles, it may not belong on your A-list.

Stage two: Systematic screening may beat serendipity

With your thesis defined, build a proprietary target universe. Use industry databases, market mapping, customer networks, and AI-powered screening tools to generate a long list of companies that fit your criteria.

Apply objective filters: size, growth trajectory, profitability, geographic footprint, ownership type, and preliminary strategic fit. Then score and rank using a target assessment scorecard that weights strategic fit heavily alongside financial profile, risk factors like customer concentration or regulatory exposure, cultural compatibility, and “dealability.”

This scoring discipline can help ensure you spend scarce due diligence resources on high-probability, high-value opportunities rather than every inbound inquiry or banker pitch.

Stage three: Triangulate valuation, don’t guess

Disciplined valuation can help prevent overpaying. Best practice generally combines three methods to establish a range, then overlays synergies and integration costs to calculate your walk-away price.

Discounted Cash Flow (DCF): Project realistic cash flows for 5–10 years, calculate the terminal value, and discount to present using a risk-adjusted rate. DCF encourages you to model integration costs and synergy timing, potentially helping prevent overpayment for synergies that may take longer than expected to materialise, or never materialise at all.

Trading comparables: Benchmark the target against similar public companies using EV/EBITDA or EV/Revenue multiples, adjusted for growth, margins, and scale. Understanding how to properly apply comparable company analysis in business valuation grounds valuation in current market sentiment.

Precedent transactions: Analyse multiples paid in recent comparable deals. This can reveal what strategic and financial buyers have actually paid, including control premiums.

Use all three to triangulate a valuation range. For example, if DCF suggests €80–100 million, comparables suggest €90–110 million, and precedents show €85–105 million, your fair value range might be roughly €85–105 million.

Stage four: Structure to share risk

Price is only one lever. Structure determines how risk is allocated and incentives aligned.

Earn-outs: Consider tying 15–30% of the purchase price to achieving revenue, EBITDA, or milestone targets over 1–3 years post-close. Earn-outs may be particularly useful when growth projections are aggressive, the target’s performance depends on retained management, or valuation gaps are wide.

Working-capital peg: Define “normal” working capital as the peg. At close, adjust the purchase price pound-for-pound if the actual working capital is above or below the peg.

Escrows and holdbacks: Consider retaining 10–20% of the purchase price in escrow for 12–24 months to cover breaches of representations and warranties or post-closing adjustments.

Retention packages: Identify 3–5 key employees whose departure could materially harm the business. Structure retention bonuses and employment agreements to lock them in.

When structuring deals, understanding the differences between equity and debt financing can significantly impact your risk allocation strategy.

Stage five: Due diligence as risk translation

Due diligence isn’t box-ticking. It’s translating findings into pricing adjustments, structural protections, integration priorities, and occasionally, walk-away decisions.

Structure diligence across workstreams—financial, commercial, legal, tax, technology, HR, operations—each with clear objectives, key questions, responsible owners, and “red flag” thresholds that could kill the deal or materially change terms. Understanding how to prepare early for due diligence from the buyer’s perspective can streamline this process significantly.

In tech deals, especially, don’t overlook the significance of intangible assets like intellectual property, brand value, and customer relationships during your assessment.

Maintain a risk register that logs findings, assesses impact, and proposes mitigations: price reduction, escrow increase, specific indemnity, integration workstream, or deal-killer. This register can become the foundation for final negotiation and integration planning.

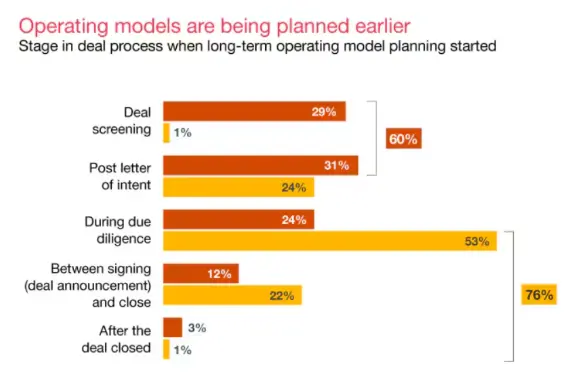

Stage six: Consider integrating before you sign

Integration is often cited as a key challenge area for acquirers. Research indicates that 60% of surveyed companies now plan long-term operating models before due diligence, up from 25% in 2019, directly wiring integration assumptions into valuation models and deal terms.

Image Credit: PwC

Early integration planning can produce three benefits:

Realistic valuation: When you map integration complexity before the LOI, you can model synergy capture more accurately. Revenue synergies might take 18 months, not six. IT integration might cost €5 million and require 12 months of dual-run, not €1 million and 90 days.

Better deal terms: If your pre-signing assessment reveals high risk—disparate tech stacks, incompatible cultures, overlapping customers—you may have leverage to negotiate earn-outs, retention packages, and seller transition commitments.

Faster value capture: With a 100-day plan built before signing, Day 1 can launch more smoothly. Employees know their roles, customers hear consistent messages, systems connect, and quick wins may be executed in the first 30 days. For detailed guidance on executing this phase, explore strategies for successful post-merger integration.

The 2026 landscape: Why discipline may matter more than ever

More than 80% of surveyed private equity and corporate dealmakers expect increased deal volume in 2026. For mid-market acquirers, this could create opportunity: potentially ample small and medium deals for prepared buyers with strong cash flows and scalable models.

AI appears to be accelerating strategic change, pulling forward decisions on scale, capabilities, data, and talent. This may reward acquirers with clear capability theses and create challenges for those chasing “AI deals” generically.

Based on historical patterns, successful acquirers may not be those who do the most deals. They may be those who do the right deals, repeatably, with a playbook that can help turn M&A from an episodic gamble into a repeatable capability.

Interested in building your buy-side playbook? Acquinox Advisors specialises in guiding strategic acquirers through every stage of the process: from target identification and valuation to negotiation and post-acquisition integration. Contact our team to discuss your acquisition strategy or explore our comprehensive M&A advisory services.

Frequently Asked Questions

How long does the typical buy-side M&A process take?

A typical middle-market transaction generally takes 6–12 months from target screening to close. Timelines can vary significantly based on deal complexity, regulatory requirements, and other factors. Early integration planning during diligence may help shorten post-close value capture timelines.

What are the most common deal-killers in due diligence?

Commonly cited triggers include customer concentration that buyers deem excessive, undisclosed liabilities, revenue quality issues, key-person dependency, IP ownership gaps, regulatory or compliance failures, and financial restatement needs. Each should typically trigger a GO/NO-GO decision based on the specific circumstances.

How can smaller corporate acquirers compete with private equity for targets?

Strategic acquirers may have several advantages: ability to pay for synergies, speed and certainty, strategic vision for the target, and cultural fit. To compete effectively, consider moving quickly, offering clean terms, articulating a compelling vision, and building relationships early.

This article has been prepared by Acquinox Advisors using data from public sources as linked. This content is for informational purposes only and does not constitute financial, legal, or investment advice. Readers should consult qualified professional advisers before making business sale decisions.